USDA Loan vs Conventional Loan: Which Is Best for Your Dream Home?

Are you considering buying a home in a rural or eligible suburban

area and exploring your mortgage options? The variety of available

loans can be overwhelming, leaving you unsure which best fits your

needs. One excellent option to consider is a USDA loan, supported by

the United States Department of Agriculture. These loans offer

significant benefits for eligible borrowers, particularly those

interested in purchasing a home in designated rural communities.

Are you considering buying a home in a rural or eligible suburban

area and exploring your mortgage options? The variety of available

loans can be overwhelming, leaving you unsure which best fits your

needs. One excellent option to consider is a USDA loan, supported by

the United States Department of Agriculture. These loans offer

significant benefits for eligible borrowers, particularly those

interested in purchasing a home in designated rural communities.

This comprehensive guide breaks down everything you need to know about USDA loans, a specific type of mortgage designed to assist individuals in rural areas. We'll also compare them with other popular loan programs, such as FHA, VA, and Conventional loans. By the end of this article, you'll have a deeper understanding of USDA loans' advantages, eligibility requirements, limitations, and how they stack up against these other common mortgage options.

Key Takeaways

-

USDA loans offer specific advantages for rural homebuyers, including no down payment and competitive interest rates.

-

Eligibility for USDA loans focuses on income limits, rural property location, and creditworthiness.

-

Comparing USDA loans to Conventional, FHA, and VA loans is crucial for deciding which loan type is best for you.

-

Your financial health, property location, and specific loan terms will be critical in selecting the most appropriate mortgage.

This article will help you understand how to compare these loan options and ultimately guide you in choosing the best financing route for your home purchase.

What Are USDA Home Loans?

The U.S. Department of Agriculture created the USDA home loan program to promote homeownership, support economic development, and improve the quality of life for rural Americans. These loans are part of the USDA Rural Development Program and are specifically designed to assist low- and moderate-income individuals and families in purchasing a home with favorable terms.

Unlike many traditional loans, USDA loans often do not require a down payment, making them one of the most accessible loan types for qualified borrowers. This can be a considerable advantage, especially for first-time homebuyers or those without significant savings for an upfront payment.

Types of USDA Loans

The USDA loan program is divided into three main types, each serving different financial and situational needs:

-

Single-Family Housing Guaranteed Loan Program: This program is for low-to-moderate-income borrowers who want to live in a USDA-eligible rural area. Private lenders issue these loans, but the USDA guarantees a portion, reducing the lender's risk and resulting in more favorable terms for the borrower.

-

Single-Family Housing Direct Loan Program: This option is designed for very low- and low-income borrowers. The USDA directly issues these loans, making them available to those who may not qualify for other financing options. Interest rates and loan terms are often highly favorable to help make homeownership affordable.

-

Single-Family Housing Repair Loans and Grants (Section 504 Home Repair program): These loans and grants are intended to help eligible low-income homeowners in rural areas improve or modernize their homes. They can also be used to make repairs to remove health and safety hazards, enhancing safety and livability.

Each loan type offers different benefits and serves various groups, but all aim to promote rural homeownership through options like the USDA mortgage programs.

Eligibility Requirements for USDA Loans

To qualify for a USDA loan, you must meet several key requirements, including income limits, property location requirements, and credit qualifications. Understanding these criteria will help you determine if a USDA loan is a viable option for you.

1. Income Limits

One of the key eligibility factors for a USDA loan is your household income. The USDA sets income limits that vary depending on location and household size. Your household income must typically fall within your area's low- to moderate-income range, ensuring these loans assist families and individuals truly needing affordable housing.

-

Low- to Moderate-Income Levels: USDA loans are generally available to individuals and families whose household income does not exceed 115% of the median income in their area. Specific income limits vary by county and state, so it’s essential to check the USDA’s income eligibility tool to confirm if you qualify based on your household size and income.

2. Property Location

Another critical eligibility factor is the location of the property you wish to purchase. The USDA program is designed to support homeownership in rural and eligible suburban areas. As a result, the property must be in a USDA-designated rural area. The USDA offers an online tool to check if a specific property is in an eligible area.

-

Rural and Suburban Locations: The definition of "rural" can vary, but USDA loans are typically available in areas with a population of 35,000 or fewer people. These areas may include towns, small cities, and regions on the outskirts of larger metropolitan areas.

3. Creditworthiness

While USDA loans often have more flexible credit requirements than some conventional loans, you must still demonstrate creditworthiness. A credit score of 640 or higher is generally recommended, though borrowers with lower credit scores (e.g., 580 and above) may still qualify depending on their overall financial profile and compensating factors.

-

Credit History: The USDA looks for a steady credit history and the ability to repay the loan. While lower credit scores may not disqualify you, a score above 640 typically streamlines the process and increases your chances of securing more favorable loan terms.

4. Homebuyer Status

To be eligible for a USDA loan, you must be a U.S. citizen, U.S. non-citizen national, or permanent resident, with proof of legal residency required. You must also agree to use the home as your primary residence; investment properties or vacation homes do not qualify under the USDA loan program.

Benefits of USDA Loans

USDA loans provide numerous benefits for eligible borrowers, making them a desirable option for rural homebuyers. Here’s a breakdown of the key advantages:

1. No Down Payment

Perhaps the most significant benefit of a USDA loan is that you can get one with no down payment. This feature is particularly appealing to first-time homebuyers or those without substantial savings. With most other loan types (like Conventional or FHA), buyers must put down anywhere from 3% to 20% or more of the home’s purchase price.

-

Zero Down Payment: USDA loans allow you to finance 100% of the home’s value, significantly lowering the upfront costs of purchasing a home.

2. Low Interest Rates

Because the USDA guarantees a portion of the loan, lenders are more willing to offer competitive interest rates. These lower rates can translate into significant savings over the life of the loan when compared to other financing options, where higher interest rates are standard, especially if you have a smaller down payment or lower credit score.

3. Flexible Credit Requirements

While USDA loans still require you to demonstrate creditworthiness, they are generally more flexible than conventional loans. If you have a lower credit score or a less-than-perfect credit history, you may still be able to qualify for a USDA loan. This flexibility makes homeownership accessible to more buyers who might otherwise struggle to secure financing.

4. Affordable Mortgage Insurance

Like many government-backed loans, the USDA's mortgage insurance fees are generally more affordable than the private mortgage insurance (PMI) required on conventional loans. This helps keep your monthly payments lower and contributes to the loan's overall affordability.

-

Lower Fees: USDA mortgage insurance includes an upfront guarantee fee and an annual fee, which are typically lower than PMI costs for borrowers with less than 20% down on conventional loans.

Limitations of USDA Loans

While USDA loans offer many benefits, they also have certain limitations that may make them unsuitable for some buyers. Here’s a look at the critical drawbacks:

1. Location Restrictions

USDA loans are exclusively for homes in rural or eligible suburban areas. This means if you're looking to buy in a more urban setting, a USDA loan won't be an option for you. The USDA's mission to support rural development means buyers in densely populated areas will need to explore other financing, such as FHA or conventional loans.

-

Eligible Areas: The USDA generally defines eligible areas as those with populations under 35,000. While this covers many small towns and some suburbs, it typically excludes larger cities and their immediate surroundings.

2. Income Limits

USDA loans have strict income limits based on your household size and the area you’re buying in. This ensures that the program is used primarily by low- to moderate-income families. If your income exceeds the USDA limits for your area, you won’t qualify for the loan, even if the home is located in an eligible rural area.

-

Household Income Cap: The USDA sets income limits that vary by county and household size. It’s essential to check your income eligibility using the USDA’s online tool.

3. Property Usage

USDA loans are strictly for primary residences, meaning you must live in the home you purchase full-time. You cannot use a USDA loan to buy an investment property, second home, or vacation property. This limitation makes USDA loans less attractive to buyers looking for a home to rent out or use as a seasonal retreat.

4. Loan Limits (Implicit)

Although USDA loans don’t have an official maximum loan amount, the amount you can borrow is based on your ability to repay the loan, which is determined by your debt-to-income ratio. This can effectively limit your borrowing power in more expensive real estate markets, where homes may cost more than the amount the USDA will approve based on income and debt levels.

-

Debt-to-Income Ratios: The USDA evaluates your debt-to-income ratio to determine how much you can afford to borrow. If you want to buy in an area with higher home prices, you may need to explore other loan options.

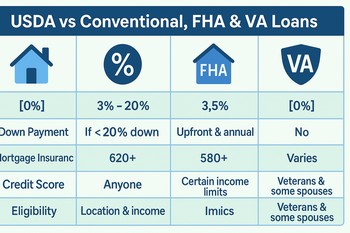

USDA vs. Conventional Loans

Conventional loans are the most common type of home financing in the U.S., and it's essential to understand how USDA loans compare. Here’s a closer look at the key differences:

Down Payment Requirements

A critical difference between USDA and conventional loans is the down payment. USDA loans offer no down payment, making them ideal for buyers with limited savings. In contrast, conventional loans usually require a down payment ranging from 3% to 20% or more, depending on the lender, the borrower’s credit score, and other factors.

Credit Score Requirements

USDA loans offer more leniency when it comes to credit scores. While a score as low as 580 might qualify, lenders generally prefer a score of 640 or higher. Conventional loans typically require a credit score of at least 620 to qualify, and borrowers with lower scores often face higher interest rates.

Mortgage Insurance

USDA loans require both an upfront guarantee fee and an annual fee. In contrast, if you put less than 20% down on conventional loans, you'll typically need private mortgage insurance (PMI), which can significantly increase your monthly mortgage payments.

USDA loan fees are typically more affordable compared to Private Mortgage Insurance (PMI) on conventional loans. PMI can become a significant financial burden, especially for borrowers making smaller down payments.

USDA vs. FHA Loans

USDA and FHA loans are both government-backed mortgage programs designed to help borrowers who may not qualify for conventional loans. Both programs have benefits, but distinct differences set them apart.

Down Payment Requirements

USDA loans are celebrated for their zero down payment, making them highly accessible to buyers without significant savings. In contrast, FHA loans require a minimum down payment of 3.5%. While FHA's requirements are relatively low compared to conventional loans, they cannot compete with the USDA’s no-down-payment option for eligible borrowers.

Mortgage Insurance

Both USDA and FHA loans require mortgage insurance, but their structures differ. USDA loans have an upfront guarantee fee and an annual fee. In contrast, FHA loans require an upfront Mortgage Insurance Premium (MIP) and a yearly MIP. FHA mortgage insurance can often be more expensive long-term, particularly with a smaller down payment.

Property Eligibility

USDA loans are specifically for rural and eligible suburban areas, meaning the property you purchase must be within a USDA-approved zone. FHA loans, in contrast, can be used to buy homes in any location, offering greater flexibility for buyers who wish to live in urban or densely populated areas.

USDA vs. VA Loans

If you're a veteran or active-duty military member, you may be eligible for a VA loan. USDA and VA loans share several similarities, including their no-down-payment feature, but they also differ significantly in terms of eligibility and mortgage insurance.

Eligibility Requirements

The primary difference between these two loan types is who qualifies. USDA loans are available to low-to-moderate-income buyers in designated rural areas. VA loans, however, are exclusively for veterans, active-duty military members, and their eligible spouses. If you meet VA loan requirements, its unique benefits might make it a better option for you.

Down Payment Requirements

USDA loans are known for their zero down payment option, which is a major advantage for buyers without significant savings. This feature is also shared by VA loans, making homeownership more accessible for eligible individuals in both programs.

Mortgage Insurance

One of the most significant advantages of VA loans is that they don't require mortgage insurance. USDA loans, however, require both an upfront guarantee fee and annual mortgage insurance fees. This difference can make VA loans more affordable over time for eligible veterans.

How to Select the Right Loan for Your Needs

Choosing the right loan is a critical step in the home-buying process. It depends on several factors, including your financial situation, the property's location, and the loan's specific terms. Here's a step-by-step guide to help you select the best loan for your needs:

1. Assess Your Financial Situation

Start by taking an honest look at your finances. Consider your income, credit score, savings, and monthly expenses. This will help you determine what kind of loan you can afford and which options are available to you.

-

Limited Savings: If you have little to no savings for a down payment, USDA, VA, or FHA loans might be your best option, as these loans offer low or no down payment requirements.

2. Evaluate Property Eligibility

If you’re considering a USDA loan, it’s crucial to check whether the home you’re interested in is in a USDA-eligible area. The USDA provides an online tool to help you determine if a property qualifies.

-

Location Flexibility: For VA and FHA loans, you have more flexibility in choosing a home’s location since these loans are not restricted to rural areas like USDA loans.

3. Compare Loan Terms and Benefits

Take the time to compare interest rates, repayment terms, and fees from different lenders. USDA loans typically offer competitive rates, but FHA, VA, and Conventional loans may also provide competitive rates depending on your specific situation.

-

No Mortgage Insurance: If you’re a veteran, a VA loan might be the most cost-effective option since it does not require mortgage insurance, unlike USDA and FHA loans.

4. Think Long-Term Costs

Beyond the initial terms, think about the long-term costs of the loan. While USDA loans offer affordable insurance premiums, VA loans save you from paying mortgage insurance altogether. If you’re eligible for both, this could be a deciding factor for your overall savings.

Conclusion: Making an Informed Decision

Choosing the right loan is a critical step in the home-buying process. After exploring USDA loans and comparing them with Conventional, FHA, and VA options, you now understand what each program offers.

Thanks to their no-down-payment option and competitive interest rates, USDA loans are a strong benefit for rural buyers with limited savings. However, for eligible veterans, VA loans might be the better choice due to their lack of mortgage insurance requirements.

As you move forward, carefully consider your financial situation, the property location, and the specific terms of each loan. With the correct information, you can make a decision that aligns with your homeownership goals and financial well-being.

Remember, thorough research, careful comparison, and understanding your unique circumstances are the key to finding the best loan. Whether you choose a USDA loan or another type, the right choice will help you achieve your dream of homeownership and financial security.

Connect With Us

Please share – it really helps